It is all about how much you keep after taxes – not what you earn from your job, a business or investments. While it is always great to see fabulous investment gains, the only financial metric that really matters is what is in your bank account at the end of the day. One of the ways you can influence this is by minimizing the taxes you pay on your investments.

It is all about how much you keep after taxes – not what you earn from your job, a business or investments. While it is always great to see fabulous investment gains, the only financial metric that really matters is what is in your bank account at the end of the day. One of the ways you can influence this is by minimizing the taxes you pay on your investments.

Unfortunately, many people do not think about how taxes impact their investment returns until near the end of the year; however, you should act all year round. Taking part in investment tax planning throughout the year will give you opportunities to keep more of what you earn. Here are some rules and strategies to keep in mind.

Know When to Take Your Losses

Psychologically, many investors are averse to taking losses, holding out to “make their money back.” Instead of emotion, logic and investment acumen need to be applied here. If an investment does not have a fundamental reason to turn around, then you are better off selling it and taking a tax loss.

Losses reduce taxes on either your capital gains for the year or, when losses exceed gains, up to $3,000 on other income. Excess losses can be carried forward to future years. Plus, you will have the proceeds to reinvest in something more likely to produce a return.

Let Winners Run

Unlike long-term capital gains, short-term capital gains are taxed as ordinary income. This means your marginal income tax rate (the highest rate applied to you) can impact your investment gains.

While you should not let the tax tail wag the investment dog, ideally you want to hold a winning investment for at least a year and a day to benefit from long-term capital gains tax treatment. This means you will pay only a 20 percent maximum tax versus whatever your marginal rate is.

As with losses, the fundamentals of the investment are key. Therefore you should not sell a holding if you think the gains are at risk just to save on taxes. If you believe in the investment for the long term, then holding out for preferred capital gains treatment can be a clever idea.

Give the Gift of Appreciation

Making charitable donations you would not otherwise give is generally not a viable tax strategy. However, if you are already charitably inclined then consider donating stock or mutual funds instead of cash.

When you donate property such as stocks, your charitable deduction is based on the fair market value of the asset on the date of the gift. It is much better to do this than donate cash.

For example, if you have a stock you purchased for $35 and it is now worth $135, when you donate it you will receive a charitable deduction of $135. If you were to sell the stock first, you would have to pay tax on the $100 gains and then have only $103 to donate in cash – assuming you are in the 32 percent tax bracket. The only winner in this situation is the IRS; both you and the charity lose. This is because the charity is excluded from paying capital gains taxes on the appreciation that occurred while you owned the asset.

Hold Until You Die

This strategy does not benefit you directly, but rather your heirs. When someone inherits an asset such as real estate, stocks, bonds, mutual funds, etc., the cost basis of the asset is reset to the fair market value at the date of death.

This means that if you have stock in company XYZ that you bought for $50 and now it is worth $500, you would pay tax on the gain of $450 per share. However, your heir would pay $0 if he sold it on the day you died. If your heir continues to hold the stock, the benefit still applies as his cost basis in the stock of XYZ would reset to $500, so he will pay taxes only on gains over that amount.

Conclusion

While you should never cheat on your taxes or do anything unethical, it is foolish to pay any more than legally necessary to the IRS. Engage in investment tax planning year-round and you may see better after-tax returns and more money in your bank account.

One highlight of the recently passed Inflation Reduction Act of 2022 (IRA; HR 5376) includes modifications to what is more commonly referred to as EV credits. Specifically, Section 30D of the Act is where the most important modifications are, and where the present tax credit for electric vehicles is spelled out in the U.S. Code. There is also new stimulus for previously owned electric vehicles, industrial vehicles and “alternative fuel refueling property.”

One highlight of the recently passed Inflation Reduction Act of 2022 (IRA; HR 5376) includes modifications to what is more commonly referred to as EV credits. Specifically, Section 30D of the Act is where the most important modifications are, and where the present tax credit for electric vehicles is spelled out in the U.S. Code. There is also new stimulus for previously owned electric vehicles, industrial vehicles and “alternative fuel refueling property.”

Despite borrowing massive amounts of money, the government still needs to find ways to raise revenue to pay for new programs and spending. The current democratically controlled Congress is looking to potentially implement new social programs and a climate bill. As a way of funding these initiatives, they are considering an expansion of the Net Investment Income Tax (NIIT).

Despite borrowing massive amounts of money, the government still needs to find ways to raise revenue to pay for new programs and spending. The current democratically controlled Congress is looking to potentially implement new social programs and a climate bill. As a way of funding these initiatives, they are considering an expansion of the Net Investment Income Tax (NIIT).

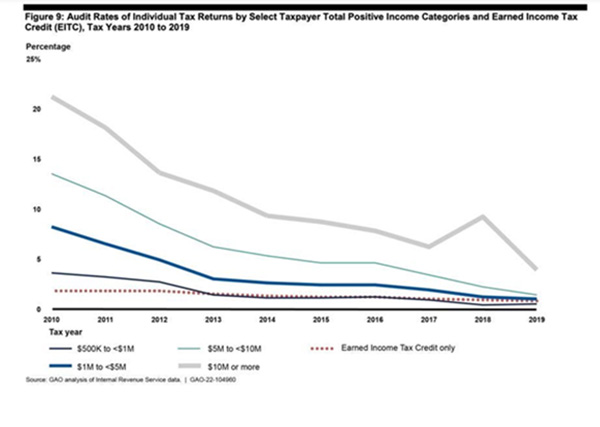

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

COVID-19 impacted the economy dramatically and commercial real estate was no exception in terms of decreased values. Often, the real property could no longer service the debt used to finance it. This debt restructuring and resulting debt forgiveness can result in taxable income.

COVID-19 impacted the economy dramatically and commercial real estate was no exception in terms of decreased values. Often, the real property could no longer service the debt used to finance it. This debt restructuring and resulting debt forgiveness can result in taxable income.

At the very end of March, the House of Representatives passed a version of the bill known as Secure 2.0. The bill passed the House with overwhelming bipartisan support in a 414-5 vote. The House version still needs to pass in the Senate, where there are differing ideas on exactly what the bill should contain. There is strong support, so it is less of a question of if Secure 2.0 will become law than what exact version.

At the very end of March, the House of Representatives passed a version of the bill known as Secure 2.0. The bill passed the House with overwhelming bipartisan support in a 414-5 vote. The House version still needs to pass in the Senate, where there are differing ideas on exactly what the bill should contain. There is strong support, so it is less of a question of if Secure 2.0 will become law than what exact version.

The IRS is currently suffering a severe backlog in processing returns from 2021 for the 2020 tax year. As of Dec. 31, there were still more than 6 million unprocessed individual returns with notices and pending refunds. There are a few things every taxpayer should know that can help them navigate any delays in filing or speeding up the process to make filing this year as smooth as possible.

The IRS is currently suffering a severe backlog in processing returns from 2021 for the 2020 tax year. As of Dec. 31, there were still more than 6 million unprocessed individual returns with notices and pending refunds. There are a few things every taxpayer should know that can help them navigate any delays in filing or speeding up the process to make filing this year as smooth as possible.

The taxation of legal settlements and fees is a complex topic. While the mechanics to make a proper claim are now easier, the rules are still complex. Below we look at six rules to consider when it comes to the taxation of legal settlements and the deduction of legal fees on your taxes.

The taxation of legal settlements and fees is a complex topic. While the mechanics to make a proper claim are now easier, the rules are still complex. Below we look at six rules to consider when it comes to the taxation of legal settlements and the deduction of legal fees on your taxes.

No one knows for sure what 2022 will bring in the form of tax legislation, but there is certain to be some action. Top tax analysts think there are several topics that are likely to come up in 2022. Most predict that a lot of potential changes that were discussed but never made much traction in 2021 will be revisited.

No one knows for sure what 2022 will bring in the form of tax legislation, but there is certain to be some action. Top tax analysts think there are several topics that are likely to come up in 2022. Most predict that a lot of potential changes that were discussed but never made much traction in 2021 will be revisited.

Self-directed IRAs (SDIRAs) are becoming more and more popular as IRA holders look to enter alternative investments. While SDIRAs can open up a world of investment options, the rules around them are complicated and compliance can be tricky. Below, we’ll look at a couple of relevant court cases that illustrate some of the potential pitfalls.

Self-directed IRAs (SDIRAs) are becoming more and more popular as IRA holders look to enter alternative investments. While SDIRAs can open up a world of investment options, the rules around them are complicated and compliance can be tricky. Below, we’ll look at a couple of relevant court cases that illustrate some of the potential pitfalls.